Little little patience is a single released by the rainmaker Majek Fashek

Shareholders have been patient for two years running, but that patience could be wearing thin.

In an unstable economy like Nigeria, cash is king. For two years running, the firm has been unable to pay a dividend because it has been running on an empty tank.

Its all the more frustrating because this company is a dominant player in its space.

Monopoly/Duopoly/Whatever form of poly with few players may be an ugly word but it is a profitable one.

There are 3 key players in the sugar space: Dangote, BUA and Flour Mills. Aggressive moves by other players mean it would lose market share at some point.

Revenue growth is not a problem

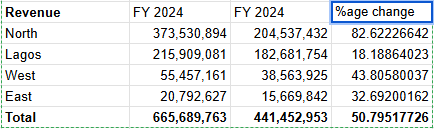

The company grew topline respectably in 2024. Full year revenue was N665 billion. Up 50% from the N441 billion it made in 2023. That comes to an average of N166 billion every quarter (a quarter is three months).

Volume details arent shared. So its hard to determine if revenue growth was driven by volume or price hikes or both.

The firm does give a geographic split. The North and Lagos account for over 80% of revenue generated during the year.

Revenue has grown at a cumulative average growth rate of 32% annually in the last 5 years.

At its current pace, the company would join the N1 trillion club in 2025 or 2026. That’s a select group of companies on the stock exchange. Members include MTN Nigeria, sister company Dangote Cement, and Seplat.

The bottomline ended in the red due to higher costs and finance charges. Loss after tax went up by 161% from N73.7 billion in 2023 to N192.6 billion in 2024.

Costs are killing

Cost of sales grew much faster than revenue. Up 78% year on year.

Gross profit declined by 63.9% year on year. From N86.3 billion in 2023 to N31.1 billion in 2024. On a percentage basis, the gross margins are abysmal.

FY 2024 gross margins were 4.6%. So for every N100 of revenue made in 2024, less than N5 was profit.

In the prior year, it was 19.5%.

Finance costs

Finance costs went up by nearly 50% year on year, driven by exchange losses on letters of credit.

A letter of credit, or a credit letter, is a letter from a bank guaranteeing that a buyer’s payment to a seller will be received on time and for the correct amount. If the buyer is unable to make a payment on the purchase, the bank will be required to cover the full or remaining amount of the purchase. I

BIPs need to earn

BIP is a short form for Backward Integration Project (BIP). For Dangote Sugar, that means home grown sugar. So rather than import sugar, sugarcane is cultivated and refined locally.

There are 3 BIPs. Located in Nasarawa, Taraba and Adamawa. From their inception till date, over $700 million has been spent. The bulk to Nasarawa and Adamawa.

In FY 2024, N5.5 billion was spent.

Management needs to provide a better timeline. When are these projects going to earn returns?

What’s the way forward?

Every 4/5/10 years you have a big bang devaluation. As long as this firm continues to import the bulk of its raw sugar, you’re going to have this scenario.

The company needs a cash infusion. The bulk of its borrowing is short term (and in a high interest rate environment, that’s killing).

Parent company, Dangote Industries Limited (DIL) DIL itself is pressed for cash. Funds had to be borrowed from the Dangote refinery (which isnt profitable yet, so why are they lending. Goes to show the squeeze DSR was in).

Buy/Sell/Hold?

Stock is a Hold for me. A hold recommendation means lets watch and see.

Losses have been declining quarter on quarter. They moved from N68.9 billion in Q1 2024 to N8.2 billion in Q4 2024. So Q1, 2025 could be a return to profit. Q1 numbers will be a rough estimate for FY 2025 performance.

The stock declined by 10% in yesterday’s trading session.

Leave a Reply