BUA Cement a couple of days ago filed its audited FY 2025 earnings. There was was decent topline and bottomline growth.

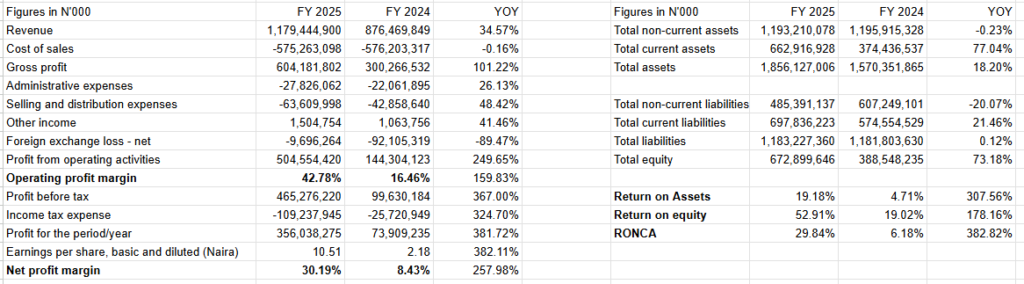

Revenue grew by 34.57% from N876 billion in 2024 to N1.1 trillion in 2025. The company joined the N1 trillion revenue club. Only a handful of companies on the NGX generate a N1 trillion or more in annual revenue.

Profit after tax more than tripled from N73.9 billion in 2024 to N356 billion in 2025.

Shareholders have cause to smile

The firm has proposed a final dividend of N10, from the N10.51 in earnings it made during the period. In essence, it will be paying all it made as profit during the priod.

Could it have pursued a different path?

While shareholders are happy with the proposed dividend, a company with such a high return on equity should have reinvested part of those profits.

An ROE of 52.91% means that for, for every N100 invested as equity, N52.91 was generated as a return

The pros and cons

Dividend investors would be quite happy with this. However, over 90% of the firm’s shares are held by founder Samad Rabiu. So in essence most of the cash goes to him.

On the flip side, in a high inflation environment, one would have been better off channeling the funds to either paying down debt.

Huaxcin’s takeover of Lafarge Africa in my opinion, is going to drive competition and margins in that space, operating margins to the point. That company will at some point in time, need cash to either dial up efficiency or sit out the eventuality of a price war.

As a blue chip firm, raising debt has and wont be an issue for the firm. Despite this, retained earnings would always be cheaper. Eating with all fingers isnt an optimal way of running a business.

Leave a Reply