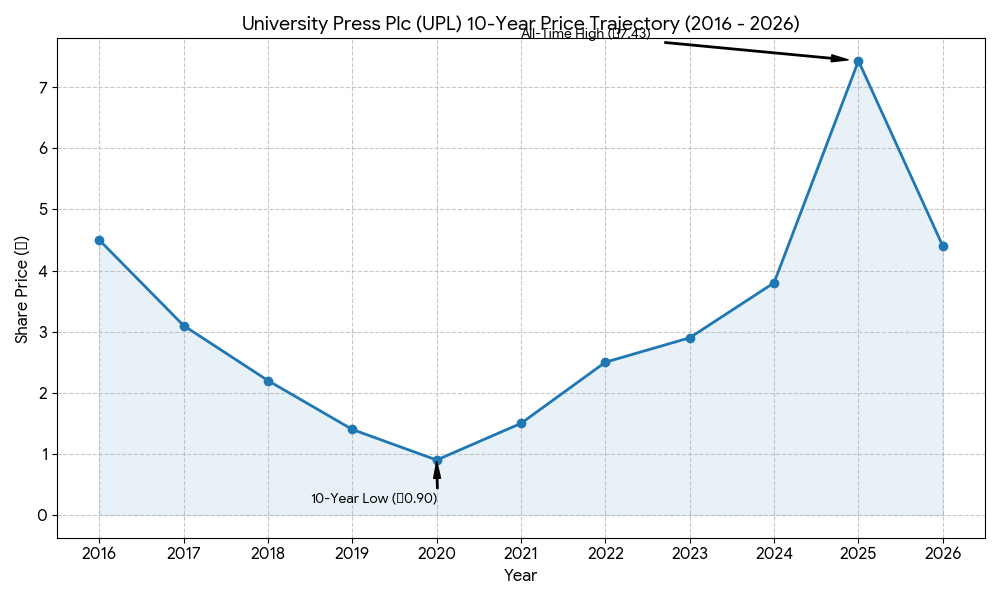

At its current price of N4.4, University Press Plc is trading at a market capitalization of N1.89 billion.

On a technical analysis basis, the stock is in a downtrend and is trading below its support level.

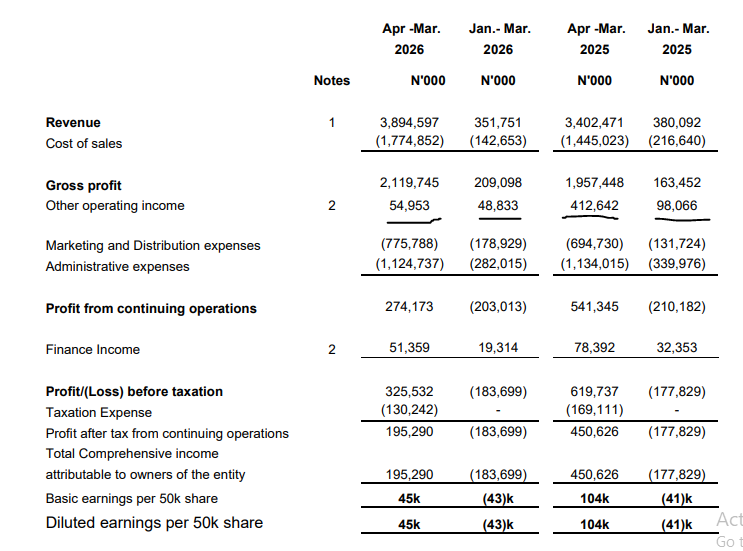

From a fundamental analysis, the interim FY 2026 numbers show a weak performance, due to a drop in other income.

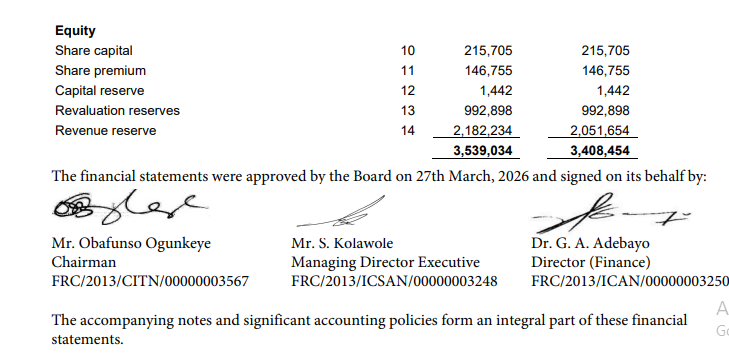

At its current price of N4.4, the stock is trading at 9.7 times earnings, more importantly, the stock is trading below its equity value of N3.5 billion.

Even if one were to discount the revaluation reserve, that would leave equity at about N2.5 billion.

Learn Africa in my opinion is the best run of the publishing stocks. In the near to mid term, this is not a high growth industry.

At bare minimum, the stock should be trading at this equity level (stripped off revaluation reserve). That would place it at a potential price of N5.79.

In percentage terms, that would be a potential upside of 31%.

Is the dividend safe?

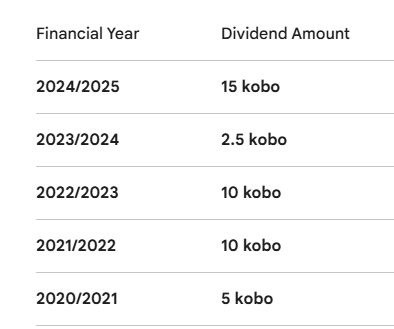

The primary reason many people hold this stock is for the dividend as the firm has a great record on that as shown above.

Maintaining last year’s dividend of 15 kobo, means the firm would need to shell out about N64.7 million. That’s a tiny fraction of its reserves.

Chances of a sharp drop in dividend are unlikely in my opinion.

What of the dividend yield?

Though the dividend yield at current price is low (in the 3.7% range), investors that have held this stock for the last 5 years should have recovered a decent chunk of their investments.

Leave a Reply